Is food inflation back?

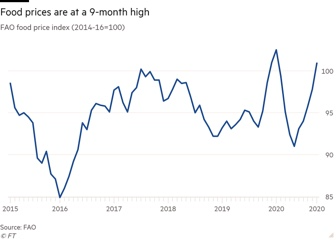

While this should come as a shock to no one, according to the Food and Agricultural Organization, global food prices were higher again in October. This marks the fifth month in a row of increases and carries the index to the highest point since January. The cereal price index climbed 7.2% from the previous month and stood 16.5% above the same month last year. The agency lowered the global cereal stocks 13.6 MMT of the prior estimate in their supply-demand forecast, taking it to 876 MMT, which is just below the record set in the 2017/18 crop year. By no means is this a tight situation, and at 31.1% stocks to usage ratio, would suggest there will be ample supplies around the globe. If it is in the right place, at the right time, is another question, though.

Australia is trying to do its part to keep food prices down and production up as they are forecast to harvest a record or near-record wheat crop this year. The Australian Bureau of Agriculture and Resource Economics and Sciences, understandably referred to as ABARES currently projects production of 28.91 MMT. Understandably, wheat values down under have been under pressure, and for the first time in four years, they are below Black Sea prices.

The USDA has reported a nice lineup of export sales this morning. China’s name has finally reemerged with a purchase of 132,000 MT of beans, 272,150 MT of beans were sold to unknown destinations, 206,900 MT of corn was reported as received during the reporting period for unknown destinations, and South Korea purchased 30,000 MT of bean oil.

Rains have slowed down the progress a smidge, but Zee French farmers continue to forge ahead with the planting of winter crops. Winter wheat is estimated to be 76% planted, up 10% for the week, and 13% ahead of a year ago, and winter barley is 87% complete versus 78% last year.

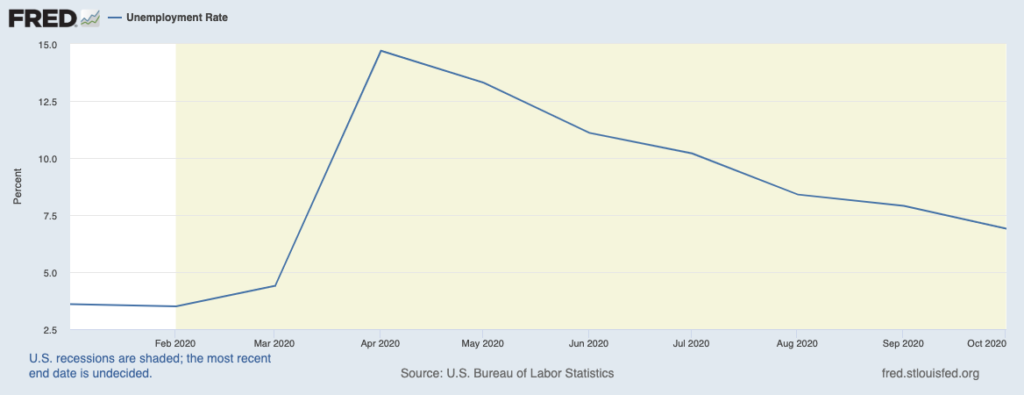

This morning, in economic news, we find that the economy added 638,000 jobs last month, which is a bit better than the 600,000 expected by economists. That said, it is well off the pace of 1.6 million we averaged for July and August and below the 672,000 in September. The unemployment rate plunged a full percentage point to 6.9%. The number of people jobless for between 5 and 14 weeks decreased by 457,000, those jobless for 15 to 26 weeks decreased by 2.3 million but those unemployed for over 27 weeks increased by 1.2 million.