From famine to feast

After nearly non-existent news yesterday, we have been confronted with a glut of reports this morning, so we might as well get started.

First, the Wheat Quality Council has finished the second day of a three-day tour in North Dakota, and as you might suspect, have found rather disappointing yields. Thus far, they have come up with an average yield of 24.6 bpa, compared with a five-year average of 42.4. It is hard to imagine things will have improved when today’s results have been tallied.

Over in Russia, the state weather bureau lowered its estimate for the total grain crop to 121 MMT, which was down 3 million from its previous estimate due to hot and dry conditions in the Volga region. Last year, this nation produced 133.5 MMT of grain.

The International Grains Council also published a few updates this morning. They lowered the U.S. wheat production number by 3.6 MMT, reduced the Canadian wheat crop by 3.8 MMT, and raised the EU output by 1.7 MMT. That said, though, they increased their estimate for global wheat estimate 1 million to 788 MMT and also bumped the global corn production estimate by 1 million to 1.202 BMT.

A bit closer to home, and indeed of great concern for the U.S. Hog Industry, there has now been a confirmed case of African Swine Fever in the Dominican Republic. This is the first known case in the Americas in forty years. As you would imagine, all pork and pork products from the Dominican Republic are now prohibited.

For the second week in a row, wheat is the only major commodity to record solid weekly sales, which came through at 515,200 MT or 18.9 million bushels. This was a 9% improvement over last week and 46% above the 4-week average. China headed up the list of buyers with 128.9k MT, followed by Mexico who took 85.6k, and then the Philippines with 59.1k. Considering we are not looking at a net reduction in corn as we did a week ago, it was undoubtedly an improvement, but one would hardly call it inspiring at 115,200 MT or 4.5 million bushels. That said, we did see an improvement for the 2021/22 crop year with sales of 529,300 MT or 20.8 million bushels. The top three purchasers were Mexico, unknown destinations, and Colombia, with 172k MT, 150k, and 129.1k, respectively. For old crop beans, we did see a net reduction of 79,300 MT or 2.9 million bushels. For the new crop, we made sales of just 312,800 MT or 11.5 million bushels. Mexico purchased 160.5k MT, China was in for 121k, and Pakistan bought 66k. Also, this morning, the USDA announced a sale of 132,000 MT of beans for the 2021/22 crop year. I will point out as well that even without any interest from China, pork sales rebounded nicely this week with a total of 38,500 MT.

Finally, 2nd quarter GDP numbers for the United States were released this morning, falling a bit short of expectations. For the quarter, the number rose 1.6%, which on an annualized basis equates to 6.5%. While that is slightly better than the 6.3% growth from the 1st quarter, economists were expecting to see a figure of around 8.5%.

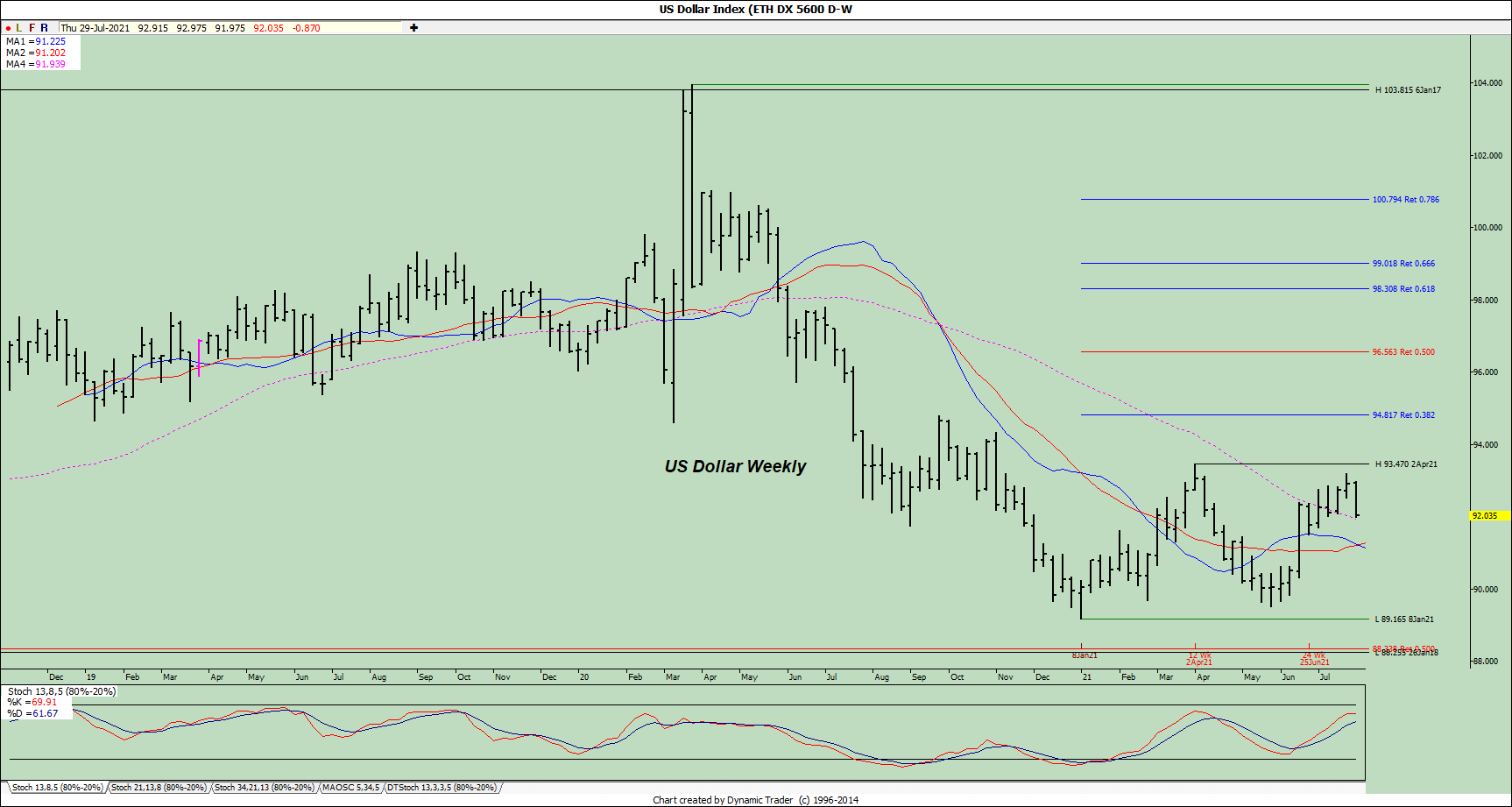

In the macros this morning, we have metals quite strong, energies higher, financial instrument soft, equities strong, and the dollar under solid pressure for the fourth day in a row. The action in that final market has not altered the long-term picture, but with the Fed not anxious to pull back on stimulus anytime soon, the intermediate picture could be turning lower.