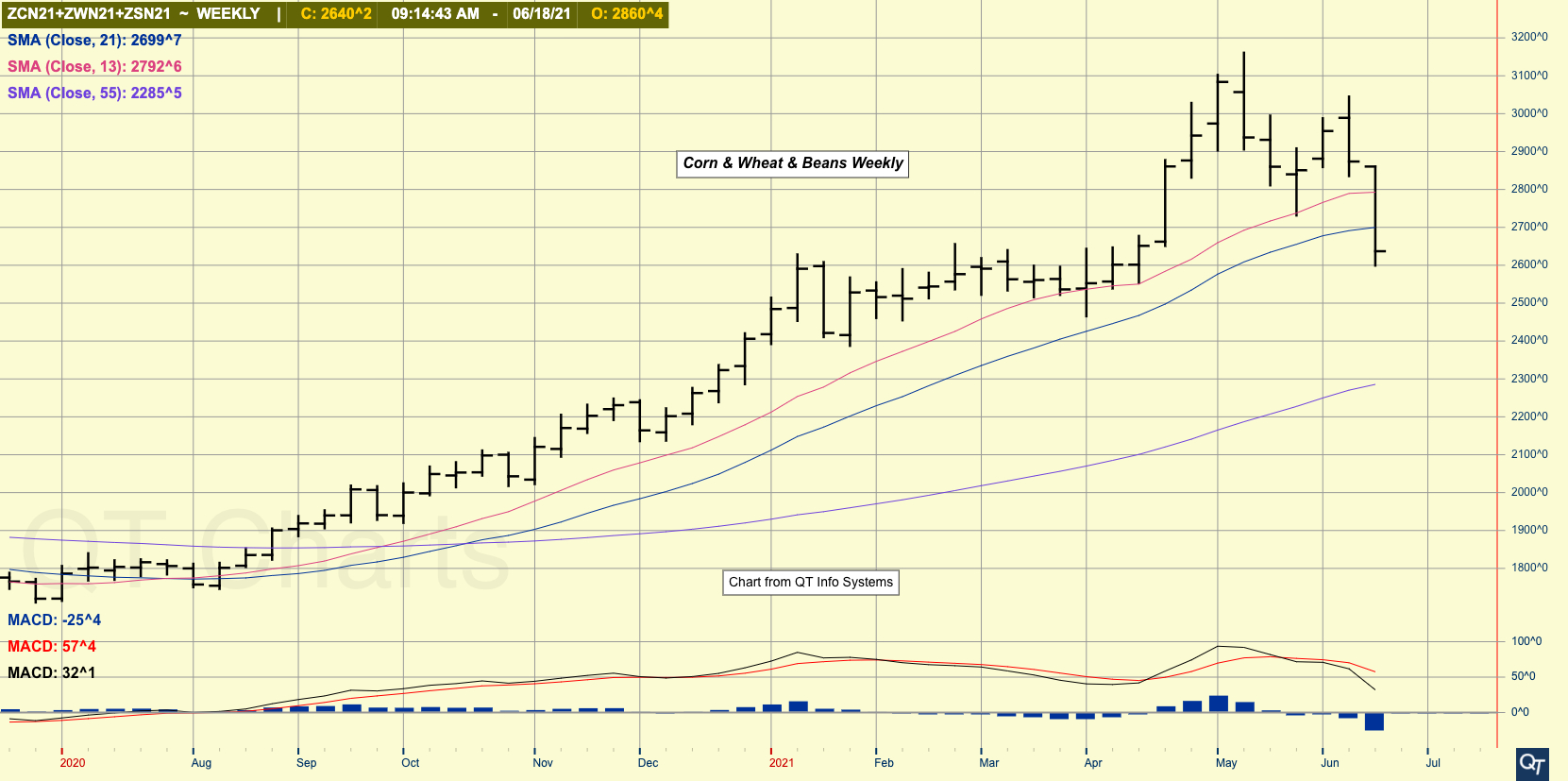

The inevitable classic panic washout

Shouting “fire” in a crowded theater, taking one step too many at the edge of a cliff, the bigger they are, the harder they fall. We can use all sorts of analogies for what occurred in the grain and soy markets yesterday. Still, we did witness a classic long liquidation panic that began to feed upon itself, and at times, the doors were just not large enough to allow the throngs of longs to exit. It was inevitable that we would witness such a day, and I suspect it will not be the last before this year is over. Many of these markets have been trending higher for the better part of a year, some reaching into record highs, and not unlike dogs, in “market years,” twelve months is roughly equivalent to seven years, which would make this run a bit long in the tooth. As I had commented several weeks back, it appeared we had found a top for this advance, but it was not until this week that we could really confirm such.

All of that said, on June 18th, it is pretty difficult to say we are not going to have a few exciting rallies ahead, as these crops are far from being made. I drove several hundred miles this week conducting a very scientific windshield crop tour, and in some areas, I had to remind myself that I was passing corn fields in northern Illinois, not pineapple plants in Hawaii. That said, with a few showers now in the past couple of days and cooler temperatures promised for, after the weekend, it is certainly not too late to witness significant improvements. If that is correct, looking forward, the next challenge for these markets will be the June 30th final acreage estimate. Seeing that we have just witnessed this breakdown, the risk of witnessing a bearish report that would send markets tumbling should be reduced significantly. If prices continue to trade sideways to lower into then, we could actually be in position for a sell the rumor, buy the fact type scenario. As I mentioned in the technical comments yesterday, we often associate the period between June 21st and 4th of July with highs in particularly the corn market, but this year, we could be developing a setup for just the opposite.

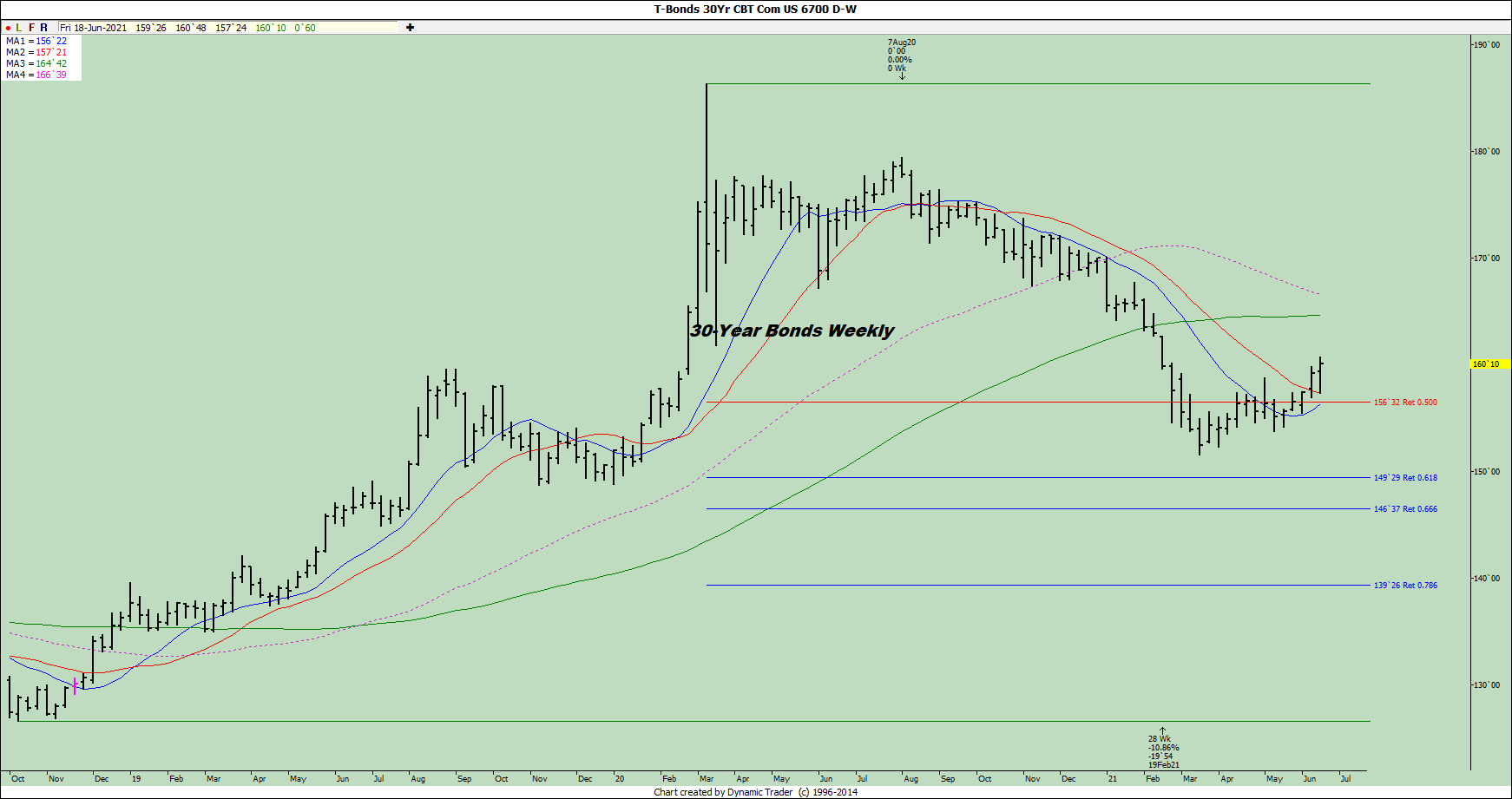

For anyone interested in keeping track of the moves for the week, if we finished the trad right now, nearby corn is down 41-cents with new down 60. Old beans are down 1.30 and new almost 1.50. Nearby wheat is down a bit over 30-cents for the week but, of course, has already been in a defensive pattern. Looking at the macros, Brent crude is now unchanged for the week, and this after reaching the highest point traded since the spring of 2019. Gold is more than $100 an ounce lower for the week and has now wiped out all last month’s rally. (Possibly canary in the coal mine?) 10-year notes are lower for the week, but 30-year bonds are at the highest level since February, possibly suggesting the Fed news was very well anticipated. The S&P 500 is down about 60 points for the week, which would not seem significant other than the fact that we have posted an outside lower week from a record high. Finally, what does appear significant is the dollar, which is up over 140 points and has long-term indicators on the cusp of turning positive.