2023 will likely go down as one of the most painful years, financially, that pork producers have ever experienced. As pork producers’ potential profits continue to erode, some economists say 2023 could turn out to be worse than 1998. The grim outlook is also unearthing concerns about what it could do to the entire pork industry, including possible contraction, restructuring and vertical integration.

According to the September Ag Economists’ Monthly Monitor, pork prices aren’t producing much optimism. Of 10 major ag commodities, the nearly 60 ag economists surveyed say they are the least optimistic about dairy, but that’s followed by pork.

When asked to list the most negative aspect of the ag economic outlook, one economist noted the extreme headwinds for pork.

“Interest rates and drought, but some areas seem to have some demand problems, like dairy and pork,” said the ag economist in the latest survey.

Related News- It’s Starting: Why Recent Processing Plant, Farm Closures Signal Major Consolidation is Now Underway for Pork and Poultry

Iowa State University’s Model for Profitability, which is shows farrow to finish operators in Iowa aren’t just losing money, forecasted 2023 margins look to be record-low.

“This is the worst annual year pork producers will ever have,” says Lee Schulz, an extension livestock economist with ISU who manages the Model for Profitability. “We always talked about 1998 as the worst year ever, but 2023, collectively, will be worse than in 1998.”

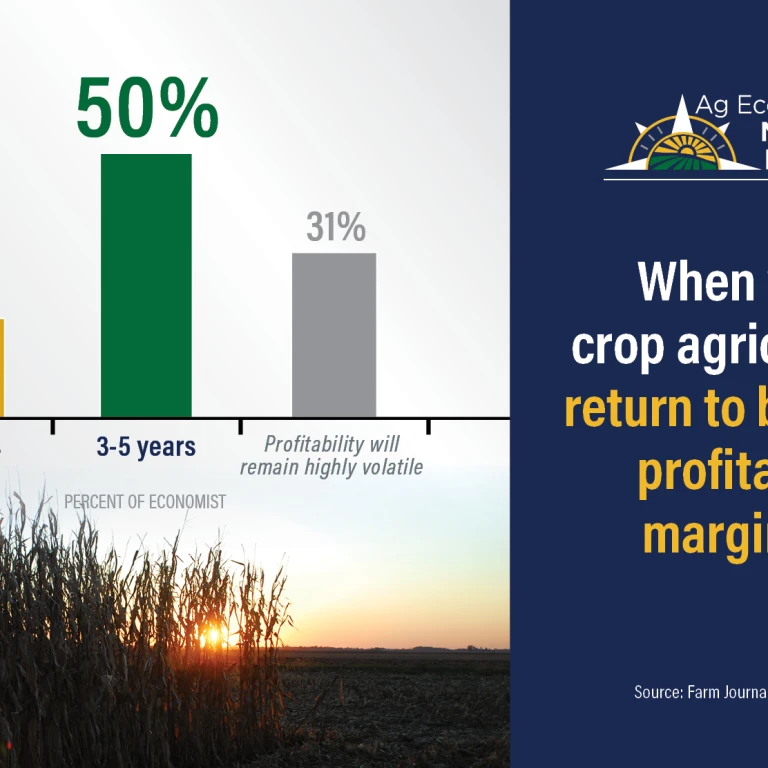

What additional changes could occur in the hog industry considering the economic challenges today? It’s a question that was asked in last month’s Monthly Monitor, and the main themes seem to be consolidation and potential fallout from Proposition 12.

The reality today is margins for hog producers could be worse than 1998, and it’s spurring what some think could be a similar situation to 1998: more consolidation in pork and poultry. Tyson Foods’ decision to shutter four poultry processing plants yet this year and into early 2024, combined with Smithfield Foods closing 35 pig farms, are strong signals consolidation is already occurring, according to ag economists.

Several economists said contraction, restructuring and vertical integration will be a direct effect caused by today’s financial woes.

“More consolidation and less opportunities for independent producers as markets for their hogs will be more difficult to find,” said one economist.

“I expect to see some reduction in the sow herd. An interesting question will be how much shrinking happens in Canada compared to the U.S.,” was another response.

Pressure from Prop 12

The other major theme was Prop 12. As the latest Monthly Monitor showed, there are severe concerns about what it will do to the marketplace.

“The hog industry possesses huge uncertainty right now,” said one economist. “Prop 12 provides an entirely new dynamic to the marketplace that’s never been seen nor experienced by any sector of the livestock industry. Moreover, it’ll have ripple effects on other industries - especially poultry and ground beef. There’ll be a shortage of pork in California and excess supplies in the other states. How will wholesalers and retailers price product - and how sharp will that influence be on hog prices? All that remains to be seen.”

What factors could impact pork prices over the next six months? That’s another question that was asked in the latest Monthly Monitor, and it all boils down to supply and demand.

“Livestock prices will largely be driven by the consumer’s economic health, determining where he/she will spend money on the meat value chain,” said one economist.

“The first thing is reduced supplies. Beef production is declining. Pork production has been equal to a year ago, so far, but the financial losses should cut production. Reduced chicken production is the likely result of low chicken prices. Tighter production sets the stage for higher prices, but consumer demand will determine if we get sharply higher prices,” another ag economist said.

For the entire livestock industry, the ag economists revealed several things that could also impact prices between now and March, including:

- Reduced supplies for beef, pork and chicken should offer price support

- Consolidation and reduction could be seen in early 2024

- Consumer economic health and demand

Pat Westhoff, director of the Food and Agricultural Policy Research Institute (FAPRI) at the University of Missouri, says it’s not just pork and dairy causing economists’ outlook to erode. The September Ag Economists’ Monthly Monitor shows lower commodity prices, concerns about demand and a negative outlook for China’s economy are all contributing to the changing views, even as the cattle herd and U.S. corn and soybean crops continue to shrink. But the most influential piece of the farm economy might be the price of corn.

“I think a lot of things are coming together to make people more pessimistic about the short-term view of things,” says Westhoff. “We’ve got lower prices for some of the major commodities, such as corn, and that’s obviously a major player in all this. Higher interest rates aren’t helping, as well. There’s just a general concern about the future of demand for U.S. agricultural products, which has probably gotten to be a more important concern this past month.”

View more results from the September Monthly Monitor.

Related News:

The One Factor That Could Make Or Break the Farm Economy Over the Next 12 Months